|

||

|

Name

Cash Bids

Market Data

News

Ag Commentary

Weather

Resources

|

Investments in Renewable Energy Are Plunging. Is It Time to Sell Plug Power Stock?/Green%20hydrogen%20by%20Scharfsinn%20via%20Shutterstock.jpg)

According to a BNEF report, U.S. renewable energy investments declined 36% in the first half of 2025, creating headwinds for hydrogen fuel cell company Plug Power (PLUG) as policies from the Trump administration reshape the clean energy landscape. The decline reflects deteriorating policy conditions following the 2024 elections, with developers rushing to lock in tax credits before year-end. Plug Power operates in the hydrogen ecosystem, which depends heavily on government subsidies and renewable energy adoption for economic viability. The company has struggled with profitability and cash flow generation, making it vulnerable to policy shifts that could reduce demand for hydrogen infrastructure and fuel cell systems. However, worldwide renewable investment hit a record $386 billion in the first half, up 10% year-over-year (YoY). Europe saw a 63% surge in investment as capital reallocated away from the U.S. market, while China maintained its dominant 44% global share.

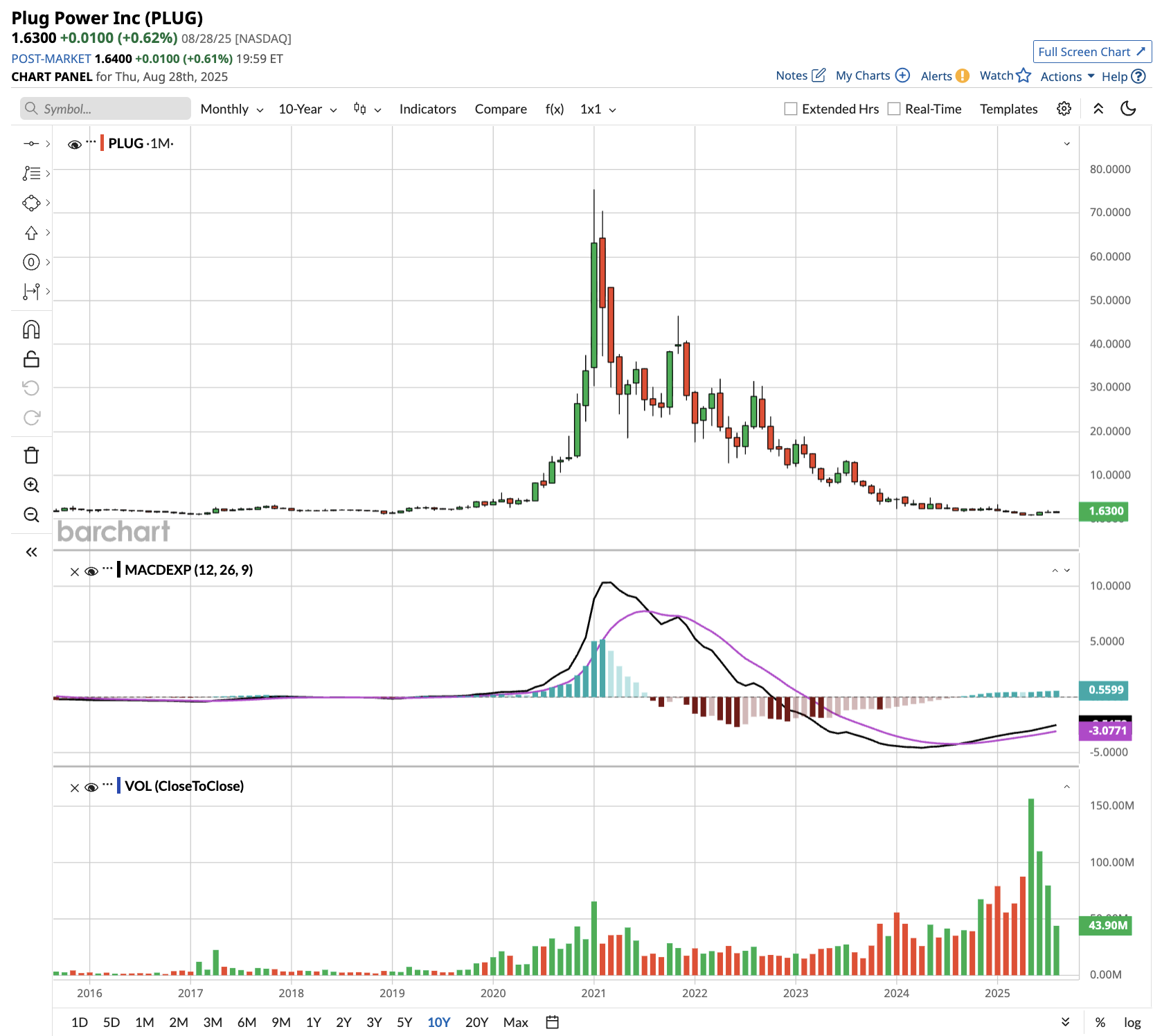

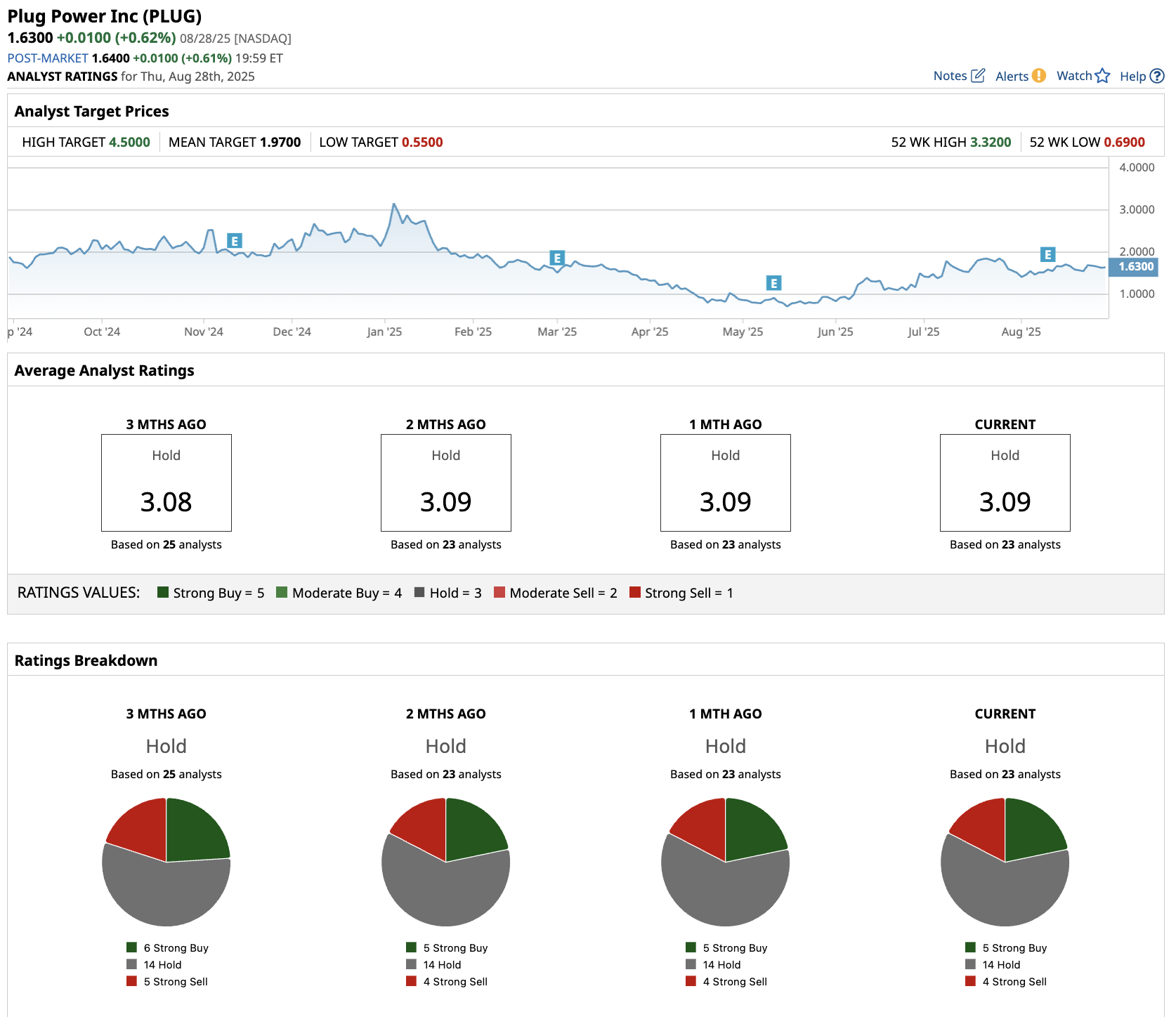

Is Plug Power Stock a Good Buy Right Now?Plug Power reported mixed results in the second quarter. It reported revenue of $174 million, a 21% increase YoY, as electrolyzer sales more than tripled to $45 million. However, the company remains unprofitable with negative gross margins of 31%, down from -92% in the year-ago period. The hydrogen fuel cell company's fortunes received a boost from recent federal legislation extending key tax credits. The 48E investment tax credit offers a clean 30% credit for fuel cell property through 2032, with no complex requirements. Moreover, the 45V production tax credit for clean hydrogen extends through 2027. CEO Andy Marsh emphasized that these policy changes provide crucial long-term certainty that was previously lacking. Operationally, Plug Power continues to execute its "Project Quantum Leap" restructuring initiative, consolidating facilities and streamlining operations to drive efficiency. The company's hydrogen production facilities in Georgia and Louisiana are performing well, with management targeting gross margin neutrality by the end of Q4 2025. Service performance improvements and pricing discipline are contributing to margin recovery. The electrolyzer business is expected to be a key driver of growth, with a robust pipeline of European projects anticipated to reach final investment decisions in 2026. International opportunities span multiple gigawatts across Australia, Europe, and Central Asia, although timing remains uncertain due to the complex approval processes required for these large-scale projects. Plug Power ended Q2 with just $140 million in cash, while its free cash outflow is forecast at $521.3 million in 2025. It's evident that Plug Power will need to raise additional capital, which will result in shareholder dilution. The company also faces tariff pressures on its material handling business, although management claims the impacts are manageable due to the reduced Chinese content in its supply chain. What Is the Target Price for PLUG Stock?Analysts tracking Plug Power stock forecast revenue to rise from $629 million in 2024 to $1.77 billion in 2029. It is predicted to end 2029 with a free cash flow of $207 million, while EBITDA is forecast at $496 million. If Plug Power stock is priced at 20 times forward free cash flow, it could more than double over the next four years. Out of the 23 analysts covering PLUG stock, five recommend “Strong Buy,” 14 recommend “Hold,” and four recommend “Strong Sell.” The average PLUG stock price target is $1.97, above the current price of $1.63. Plug Power’s success depends on government subsidies and its ability to execute on ambitious growth plans while managing cash constraints. Investors should view this as a speculative bet on the development of the hydrogen economy rather than a stable investment opportunity. The key question is whether the company can survive the U.S. policy headwinds while positioning for eventual recovery. The stock's volatility and dependence on government support make it unsuitable for risk-averse investors.

On the date of publication, Aditya Raghunath did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here. |

|

|